VolRadar is a daily options analytics platform for premium sellers — the traders running iron condors, credit spreads, cash-secured puts, and the wheel on S&P 500 names.

The pitch in one line: stop opening ten Bloomberg tabs at 9 AM. We do the morning math for you.

Every night after US market close, we pull end-of-day options data from ORATS, run it through our models, and ship a pre-market brief. By the time you sit down with coffee, you already know which tickers are worth selling and which to skip.

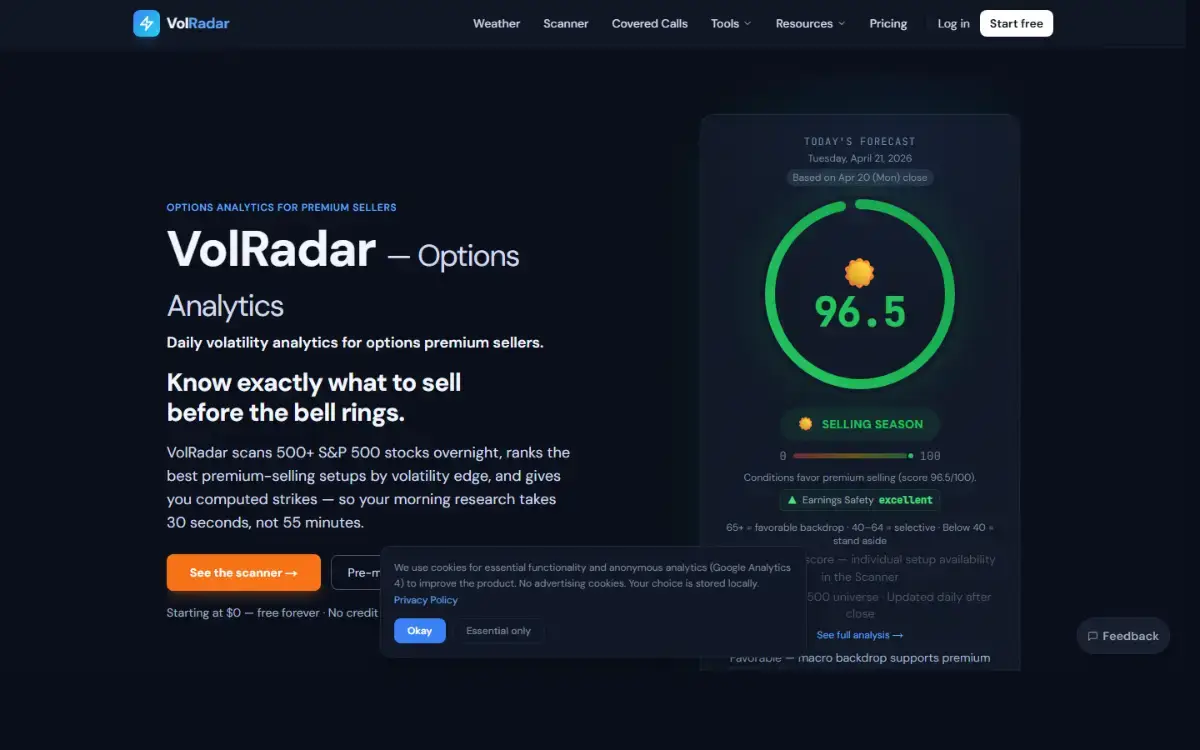

Weather Score. A 0–100 number that answers one question: is today a good day to sell premium? Five inputs — Premium Edge, VIX Regime, Volatility Trend, Earnings Safety, Term Structure — collapsed into a single signal you can act on in seconds.

What's under the hood:

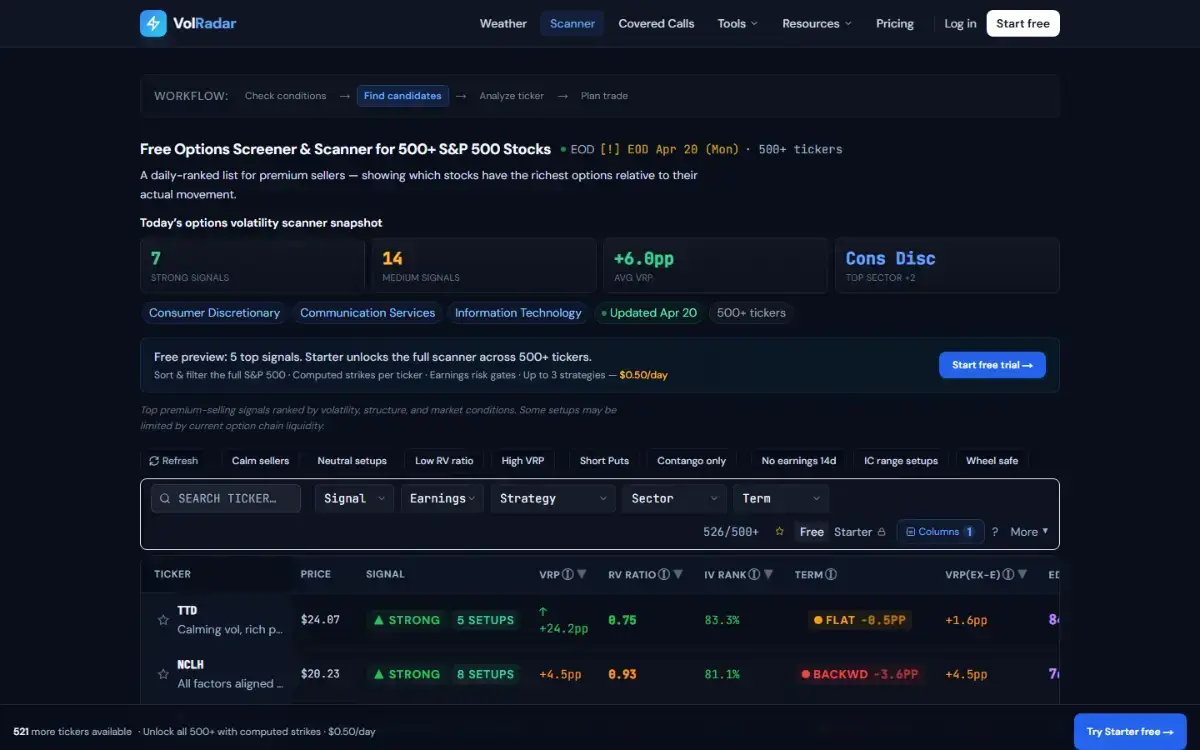

• IV Rank — 252-day lookback on 30-day ATM implied vol. Tells you if premium is actually rich or just noisy.

• VRP (Volatility Risk Premium) — 30-day IV minus 20-day realized. The tickers where option buyers are paying up for vol that doesn't show up.

• Computed strikes — target your delta or target your credit; we return the strikes that hit.

• Earnings-crush history — per ticker, the actual IV collapse after announcements. Stops you from selling "rich" premium three days before a binary event.

Coverage: 500+ US stocks and major ETFs. Data comes from ORATS's commercial feed. Updates ship daily around 6 PM ET.

Pricing. Free forever gets you the Weather Score, four calculators, and a basic scanner. Starter is $19/mo and adds the full scanner, pre-market brief, computed strikes, and weekly ideas. Founders can lock in $15/mo for life during launch.

Methodology is fully documented and open: https://volradar.com/methodology